To help meet their sustainability goals, more and more companies are signing clean energy power purchase agreements (PPAs). While long-term contracts such as PPAs can help companies hedge price risk in the long term, they may also result in significant short-term losses if not designed and monitored carefully.

Unfortunately, many corporate renewable energy buyers lack the teams or tools to carry out this kind of due diligence. But with the right mix of human expertise and purpose-built tools, companies can minimize risk and maximize the effectiveness of their PPAs.

This playbook outlines three key steps clean energy buyers should take to evaluate, monitor, and build an effective clean energy portfolio. You’ll learn how to:

Successfully monitor a project’s financial and operational performance

Forecast settlement payments to avoid costly surprises

Ensure that project locations and technology types align with your sustainability goals

Fill out the form below to access the full playbook.

A view of Q3 2024 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. Please fill out the form to access the full report, the Editor’s Note is below.

AI Introduces Unprecedented Power Needs: How Will Clean Energy Markets Be Impacted?

The landscape of U.S. power markets is being dramatically reshaped by an unprecedented wave of data center development, driven largely by artificial intelligence (AI) and cloud computing demand. The headlines are alarming: hyperscalers are announcing tens of billions of dollars of investments this year in data center infrastructure, ISOs are forecasting supply shortfalls and/or reliability concerns, and load forecasts are off the charts relative to historical growth rates.1-3

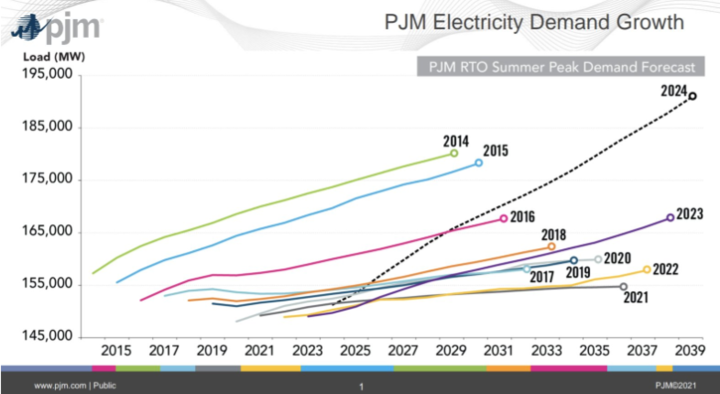

Figure 1: PJM demand growth forecast over time. Source: PJM.

With a historically reliable power supply and low-latency fiber network, the PJM region is currently a priority for digital infrastructure development – with more than 4GW already in Northern Virginia alone. PJM’s latest load forecast report forecasts a 1.6% annual growth rate for summer peak demand and 1.8% for winter peak demand, represented in Figure 1. Both growth rates are multiples larger than what we have seen historically, doubling from the estimates released last year with data center growth cited as a major contributor.

To put these numbers into perspective, summer peak demand in PJM is expected to increase above this year’s peak by almost 42GW in 2039 – representing a 28% increase. The winter peaks are forecasted to be 31% higher than last winter’s. This dramatic expansion puts grid reliability at risk, and also limits coal retirements in the next few years.2

What does this all mean for clean energy buyers or investors trying to plan for the future? Our guidance has generally fallen into one of three categories:

First, start with the historical facts on the ground.

All too often, we see forecasts – whether about future power prices, intra-day price volatility, wind/solar capture rates, congestion and curtailment, or emissions impacts – that are disconnected from historical realities. We find that this sort of discontinuity is very rarely warranted in power markets, even in a time of accelerated change (such as today).

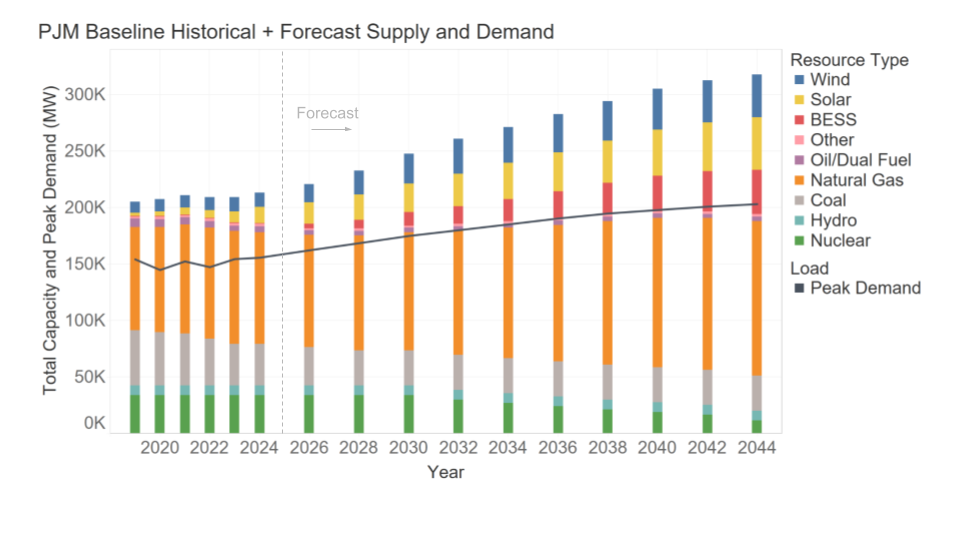

Figure 2: Historical and forecasted PJM generator capacity and peak load.

Figure 2 shows the historical and REsurety’s forecasted generation supply (colored bars) and peak load (line) in PJM. While the market will be tight over the next few years, after that we expect load growth to be more balanced with supply growth.

The result of this will be elevated prices in peak winter and summer months over the next few years, followed by smoother seasonal profiles in later years. Overall, our forecasted PJM power pries are increasing over the next 20 years in all of our modeled scenarios.

Second, get back to fundamentals.

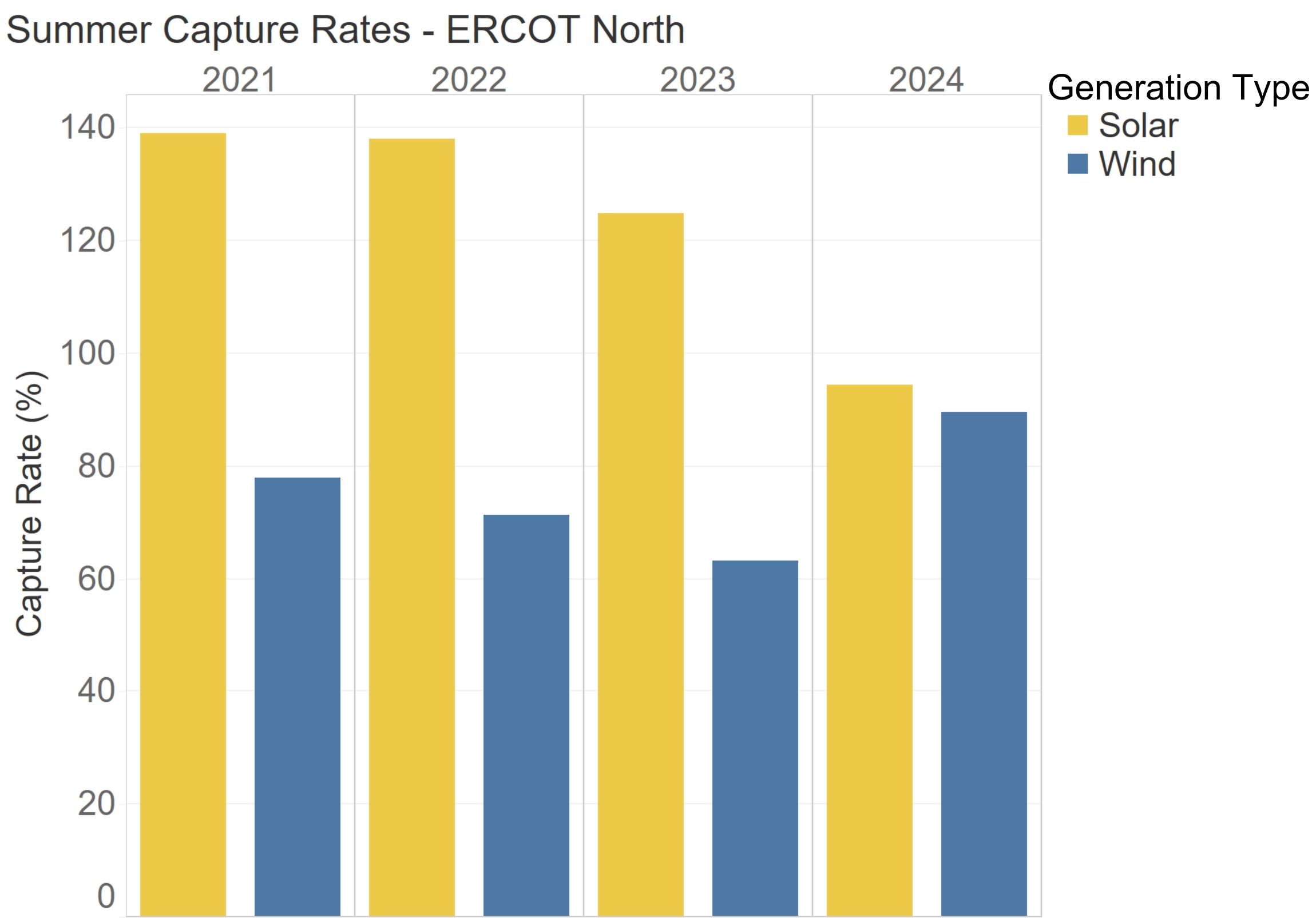

While AI-driven load growth is a new variable to consider when evaluating the future, it is not the only variable in power markets. Fuel prices, renewable energy penetration, hourly weather conditions, and congestion continue to dominate the value story for renewables, and likely will for some time. Consider solar capture rates in ERCOT this summer: while ERCOT set a new peak load (thanks in part to the 7+ GW of data centers in Texas), the summer capture rate for solar projects in Q3 hit a record low, dropping below 100% for the first time ever due to the rapid continued buildout of solar in Texas (Figure 3). Wind capture rates, meanwhile, have actually increased, as solar balances out the renewable mix. Our forecasts see this trend continuing into the future, with the average solar capture rate over the next decade at ~60%, as solar penetration continues to increase in ERCOT.

Figure 3: Summer solar and wind capture rates in ERCOT North.

Third, do not underestimate the impact of transmission.

This is relevant to multiple areas in the era of AI load growth. Data centers are increasingly struggling to get load interconnection agreements in place, causing delays and/or relocations of planned investments. This is already acting as a brake, all else equal, slowing AI-driven load growth. Additionally, congestion is on the rise, resulting in renewables getting bottlenecked and becoming undeliverable to load.

This has both financial and environmental implications: project owners and corporate offtakers with basis-sharing provisions will be financially impacted, and the emissions benefit of the clean generation will be significantly reduced. Our recent study found that 10 million metric tonnes of CO2e were emitted in ERCOT alone last year as a consequence of transmission congestion (Figure 4).4 When developing a clean energy purchasing strategy, accurately evaluating the “deliverability” of the generated clean energy is an increasingly critical consideration.

The intersection of AI-driven load growth and clean energy development presents unprecedented opportunities, but success demands strategies grounded in historical data, fundamental market drivers, and realistic infrastructure constraints – and not over-reacting to headline growth numbers. At REsurety, we remain committed to providing the analytical tools and expertise needed to navigate these complexities and make informed decisions in this rapidly evolving market landscape.

Derived from the scientific paper: Carbon Impact of Intra-Regional Transmission Congestion, which received unanimous support from the ZEROgrid Independent Advisory Initiative advisors (MIT Energy Initiative, Princeton, WattTime, and REsurety). To access the study, please scan the QR code.

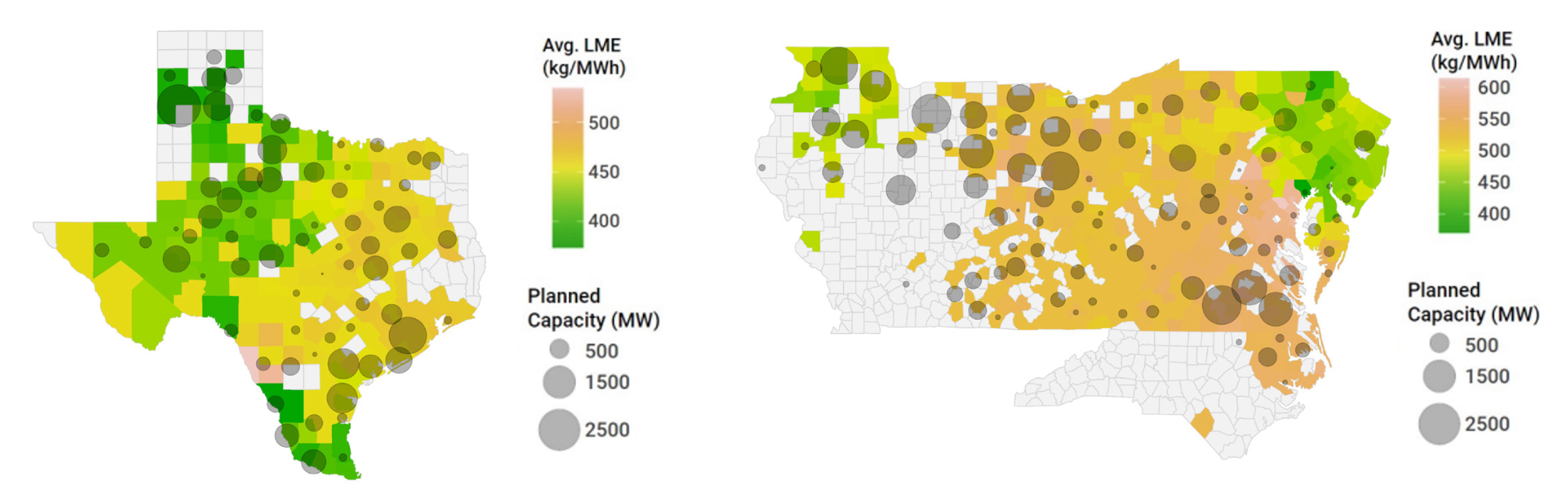

The emissions intensity of electricity can vary greatly within grid regions at any given time due to transmission congestion, yet current environmental policies and carbon accounting frameworks typically ignore these differences. By overlooking transmission constraints, these policies risk increasing system-wide emissions and worsening grid congestion, even when consumption and carbon-free energy are matched hourly. A notable portion of new wind and solar capacity proposed for ERCOT and PJM is planned in areas with substantial congestion (Fig. 1), but without significant transmission expansion, these projects will exacerbate congestion and limit emissions reduction. Through several case studies, we find that congestion-aware emissions metrics, such as Locational Marginal Emissions (LMEs), can more accurately measure the carbon impact of clean energy procurement and enhance market signals to support better grid planning and procurement strategies.

Key takeaways:

Transmission congestion has a significant impact on price and emissions for the power grid. a. For example, in 2022, transmission congestion in ERCOT increased system cost by $2.8 billion and system emissions by 13 million tonnes CO2e, which is 8.7% and 7.5% of the system total respectively.

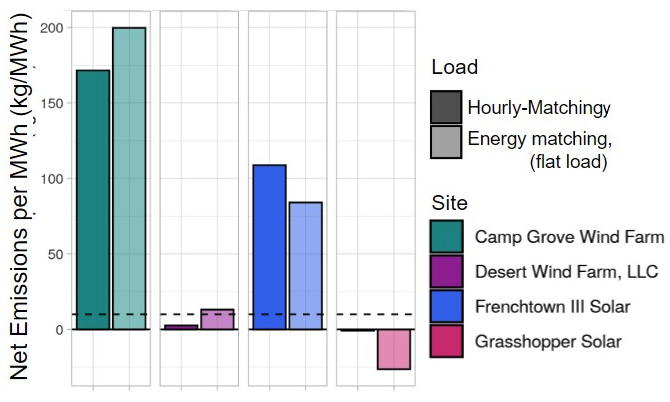

In the same grid at the same hour, different locations frequently observe a difference in emission intensity of hundreds of tonnes of CO2e due to transmission constraints. a. Even 100% hourly matched consumption with clean energy is often not carbon-free and, in many instances, hourly matching can actually increase operational emissions relative to annual matching (Fig. 2). b. Hydrogen production that complies with the current proposed 45V criteria will often significantly increase real-world emissions.

Current carbon accounting methods overestimate emissions reductions by overlooking intra-regional transmission congestion. a. Granular emission data, such as Locational Marginal Emissions rates, incorporate transmission impact, providing a more accurate measurement of the real-world carbon impact of grid connected projects.

Transmission planning and infrastructure expansion must be accelerated to achieve the decarbonization potential of renewable energy development. a. Clean energy procurement that utilizes marginal emissions rates to inform citing will better incentivize the development of projects in areas of uncongested transmission.

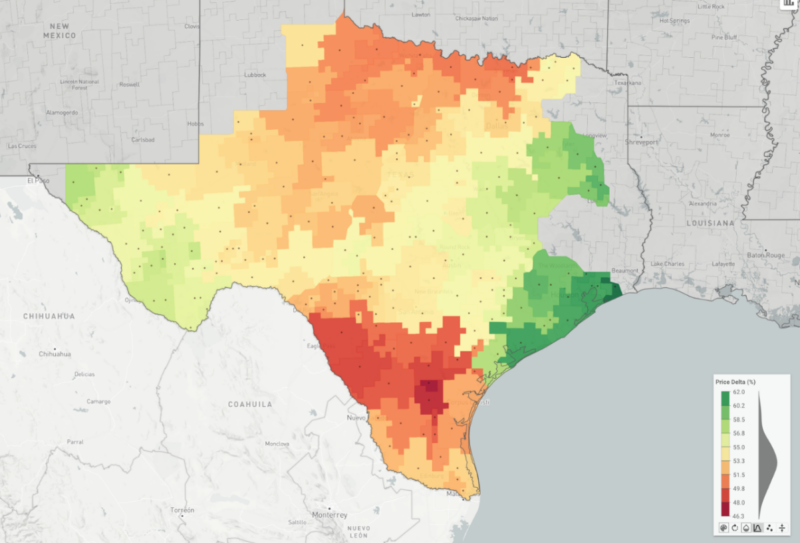

Figure 1: Contour map of 2023 average LME by county across ERCOT and PJM, with the combined wind and solar interconnection queue for each county (gray circles) overlaid.

Scope

This work uses nodal LME data for the past five years in ERCOT and PJM to quantify the effects of congestion on carbon emissions and the efficacy of annual- and hourly- matching carbon accounting frameworks. The impact of intra-regional congestion is shown to be a vital component of effective carbon accounting methods and complementary policies, and policy proposals that frequently overlook this impact risk significantly increasing real-world emissions despite the operational and cost burdens of compliance with hourly matching.

Figure 2: Map of load and procured power from four different renewable project options in PJM; 2023 net emissions from matching scenarios where both rigorously hourly-matched load through load-shifting and 100% annually-matched flat load have significant net emissions.

Assuming equal emissions and perfect generation deliverability within a grid region misses a major factor in determining the induced and avoided carbon emissions, respectively, of load and renewable generation. The induced emissions of a newly built load could be reduced by hundreds of kgCO2e/MWh just by siting it in Eastern Pennsylvania instead of Virginia, for example, and a Virginian wind farm could avoid 50% more carbon than an equivalent farm in Northern Illinois. Prioritizing and incentivizing the development of new renewable projects in less congested regions could meaningfully expedite grid decarbonization, and avoid the exacerbation of already existent congestion-driven deliverability issues.

Carbon accounting frameworks guide policy and decision-making around investments in renewable energy, making them critical to understand in the context of real-world grid operations. In the absence of empirical work assessing the effects of intra-regional congestion on carbon emissions, ongoing policy design assumes that transmission congestion within grid boundaries can be ignored. In this work, we aim to test this assumption by quantifying the frequency and severity of intra-regional congestion and its impacts on carbon emissions and prominent carbon accounting frameworks. This analysis is done in both PJM and ERCOT using nodal locational marginal emissions data. Through several case studies, we find that load that is 100% hourly-matched through load-shifting will often result in significant net operational emissions, and sometimes even increase net emissions relative to annual-matching. This work demonstrates that, in the absence of robust transmission expansion, grid-region boundaries are insufficient to ensure hourly-matching is effective. Impacts of intra-regional transmission congestion are shown to be vital components of effective carbon accounting frameworks, calling into question frequently made assumptions ignoring intra-regional congestion in studies and policy proposals.

This paper, authored by Nat Steinsultz, Pierre Christian, Joel Cofield, Gavin McCormick, and Sarah Sofia was published by IOP Science in Environmental Research: Energy, Volume 1. You can find the full paper here, or download a PDF version by clicking the button below.

Increasingly large amounts of electric supply and load are being deliberately operated or sited on the basis of marginal emissions factor (MEF) models. Validating and calibrating such models is therefore of growing policy importance. This paper uses a natural experiment involving variation in relative changes in wind generation potential at wind farms in the ERCOT power grid to create a benchmark MEF and examine the relative accuracy of several common classes of short term MEF models. This work focuses on MEFs at the level of a few individual generating nodes, a much smaller geographic scale than the Balancing Authority (BA) or load zone. Additionally, the use of wind generation potential as a regressor allows us to factor in wind curtailment, in contrast to previous work. We evaluate multiple prevalent existing MEF models and find that both dispatch and statistical MEF models have a high degree of agreement with the benchmark MEF, while heat rate and average emissions do not. We also find that the emissions reduction benefits of optimizing electricity with MEFs using a geographically granular model instead of a BA-wide model are 1.4, 1.3 and 1.5 times larger for dispatch, statistical and heat rate models, respectively.

A view of Q2 2024 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. Please fill out the form to access the full report, the Editor’s Note is below.

Maha Mapara Analyst Senior Analyst, Analytics Services

Devon Lukas Lead Analyst Associate, Analytics Services

Carl Ostridge Editor SVP, Analytics Services

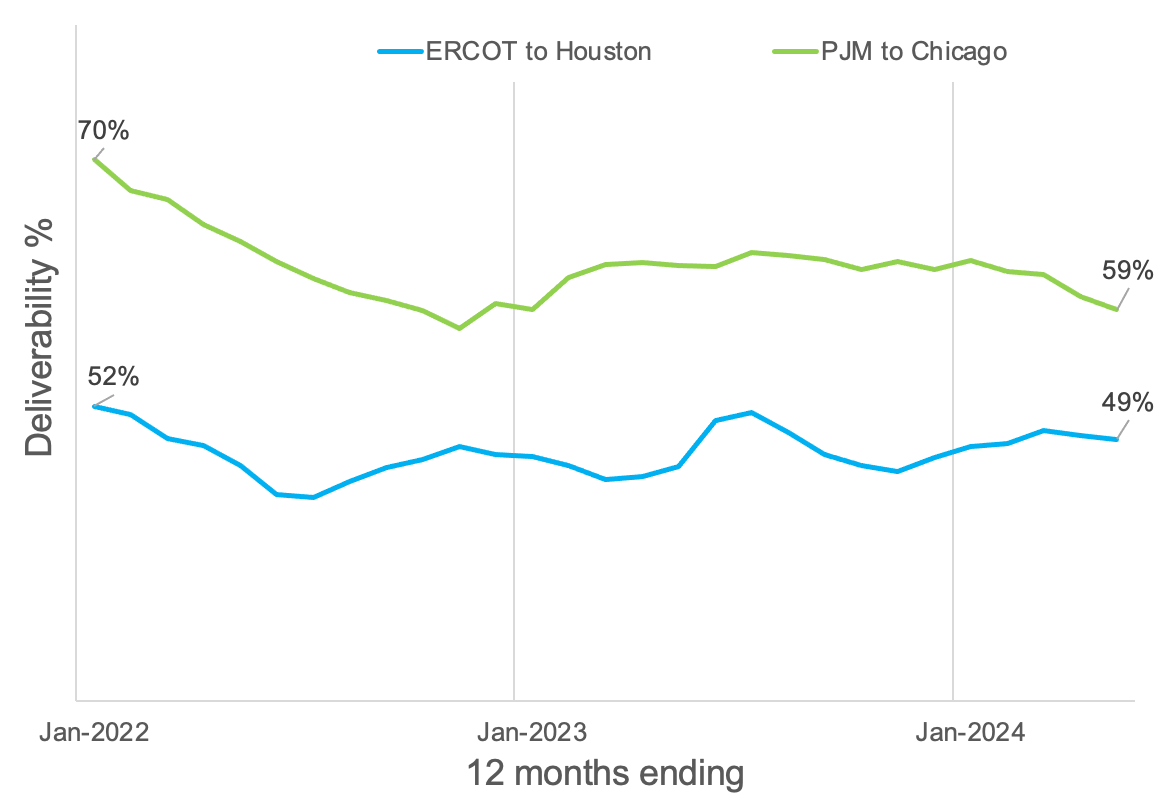

Deliverability: Can Clean Energy Reach Consumers?

Clean energy generators are the fastest growing sources of new energy on grids across the country. But if the impact of those new projects is going to be maximized, and utilized meaningfully in hourly matching carbon offset techniques, the country also needs to invest large sums in improving transmission infrastructure to get the clean energy to load centers. There have been a couple of recent announcements aiming to speed up the development of much-needed transmission (e.g. FERC Order 1920 and Department of Energy TSED funding), but how much of a problem is transmission currently?

To answer this question, we’ll use the concept of “deliverability” – in other words, how much clean energy can reach consumers in a given location. The concept of deliverability is already built into the market prices that system operators publish. There are three components to Locational Marginal Prices (LMPs); energy, congestion, and line losses. Line losses tend to contribute relatively little to the overall prices, and so we can use the difference in LMPs between two locations to estimate the deliverability of the energy. When the LMP at a generator diverges materially from the LMP at the load center, this is a sign that the location is experiencing congestion – either high prices that encourage generation, or low (even negative) prices resulting in renewable generator curtailment.

For this analysis, we’ve defined power as “deliverable” if the LMP at the generator is within 10% of the LMP at the load center. Renewable generation output during periods with greater than 10% LMP divergence is likely subject to congestion, and is therefore considered undeliverable. This is a somewhat simple metric, but it aims to boil down a complex issue into something digestible and relevant; after all, deliverability is a key component in the developing hourly matching frameworks.

In Figure 1, the 12-month trailing average of deliverability is shown for clean energy generators in ERCOT and PJM and load centers in Houston and Chicago, respectively. Historically, only between half and two-thirds of clean power is “deliverable” to these major load centers. This highlights that transmission congestion has been, and still is, a meaningful issue. It’s also notable that despite higher penetration levels of wind and solar in ERCOT, the deliverability of clean energy to Chicago has dropped more rapidly since the start of 2021.

Figure 1: Trailing 12-month average clean energy deliverability to Houston and Chicago.

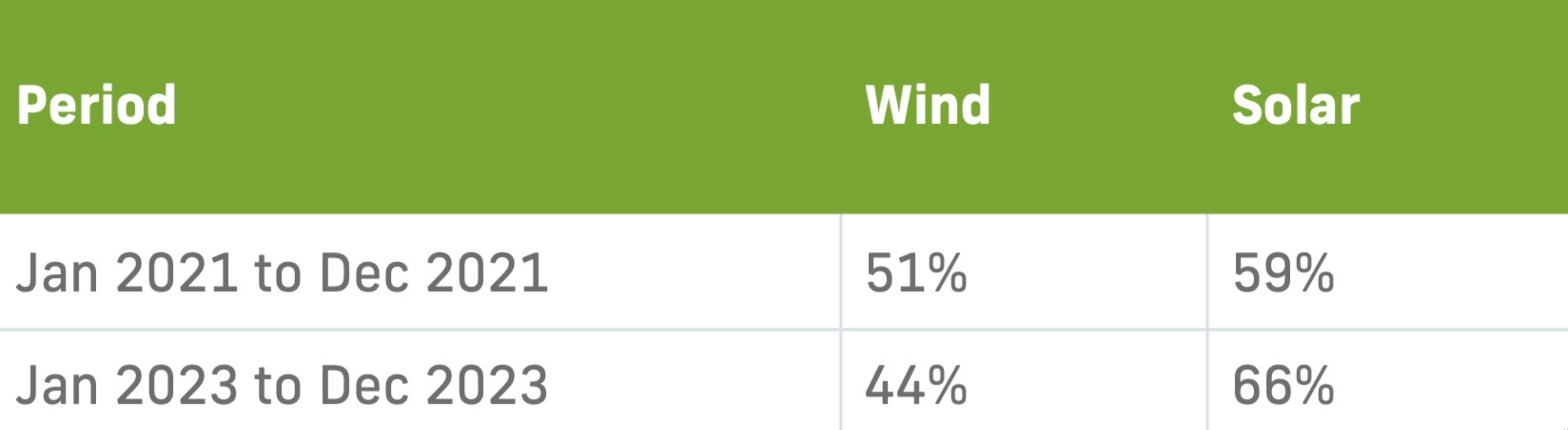

When we look a little deeper at the ERCOT deliverability, separating the results for wind and solar projects, the story of the flatter deliverability trend becomes clearer. The deliverability of wind in ERCOT has been trending downwards over the past few years, while solar has trended upwards. There are two factors in favor of solar’s better deliverability: timing and location. Solar’s on-peak generation coincides with higher load, leading to fewer congestion issues. Furthermore, the operational solar fleet is more geographically dispersed compared to the wind fleet, meaning fewer solar projects are subject to major transmission constraints (such as in the Texas Panhandle and Gulf Coast).

Table 1: Deliverability of ERCOT wind and solar energy to Houston.

Of course, these trends will evolve over time as more clean energy is added to the grid, thermal generators are decommissioned, energy storage capacity expands, gross and net load profiles evolve, and transmission either stays constant or gets upgraded. This metric is just the beginning of our efforts to analyze this complex issue. A REsurety whitepaper on deliverability is in the works, covering more regions and diving deeper into the underlying causes and resulting carbon impacts.

Over the past 10 years, voluntary procurement of clean energy by corporations has been a tremendous driver of renewable energy development. Since 2014, large companies have signed procurement contracts supporting the development of over 70 gigawatts of renewable energy in the United States,1 in addition to purchasing renewable energy certificates (RECs), providing tax equity financing, and advocating regionally and nationally for more clean energy deployment. These voluntary procurement trends are continuing to scale and expand into other markets such as Japan, South Korea, and Taiwan.2

The urgency of the climate crisis is prompting many large energy consumers to consider how they can assess the impact of various actions on grid decarbonization and reliability. Such an assessment can be best made using consequential emissions impact analysis, which employs various approaches to estimate the difference between total global emissions in different possible states of the world.

Although many authors have published on consequential emissions impact analysis, there have been different views and until now no joint statement from differing authors on areas of consensus and how to resolve discrepant conclusions.

To provide greater clarity to corporate actors, ZEROgrid created the Impact Advisory Initiative, or IAI. The IAI comprises a group of expert practitioners from the National Renewable Energy Laboratory (NREL), Princeton University, REsurety, RMI, and WattTime who collectively identified key points of consensus as well as areas requiring further research.i

This paper provides an overview of the IAI’s findings regarding emerging areas of consensus about consequential emissions impact analysis, its implications, and areas where further research is required.

Areas of Consensus:

Defining Impact. The true impact of any voluntary corporate action (or any action) is the difference in total emissions between a world where the action was taken versus one in which it was not taken.

Components of impact. This impact is the sum of several different contributing effects, which must include the effects over the lifetime of the intervention — how an intervention changes the short-run operations of power plants, and structural change, i.e., how it changes the total supply of different power plants in the long run — to fully capture the impact of an action.

Estimates versus true values. The field has a number of ways to produce estimates of total emissions impact and its components. Although there is agreement regarding how changes to short-run operations can be quantified, the field currently lacks — and indeed may always lack — any generally accepted way to empirically verify estimates of structural change. Therefore, any approach that seeks to measure total impact has (potentially significant levels of) uncertainty.

iThe ZEROgrid initiative brings together a group of corporate actors, including Akamai, General Motors, HASI, Meta, Prologis, Salesforce, and Walmart, seeking to drive deep decarbonization alongside increased power grid reliability and affordability, working in collaboration with emissions and reliability experts. Additional information is available at https://zerogrid.org/.

A view of Q1 2024 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. Please fill out the form to access the full report, the Editor’s Note is below.

Devon Lukas Lead Analyst Senior Analyst, Analytics Services

Carl Ostridge Editor SVP, Analytics Services

Record-Breaking Winter for Solar: Behind The Scenes

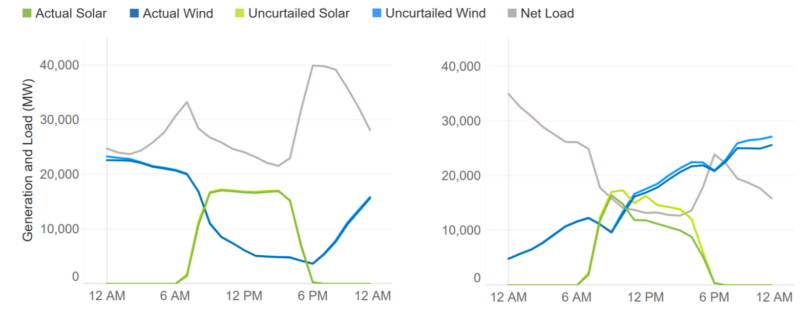

Solar output in ERCOT has been in the news as of late, with the buzz around the record-breaking 17.2 GW peak on February 19th amplified by the 18.7 GW peak on March 28th. While impressive, these records are actually not broken as often, or by as much, as one might initially expect given the amount of recent solar buildout. The current generation record would be 300 MW higher were it not for the complex interactions between the weather, transmission infrastructure, and tax incentives.

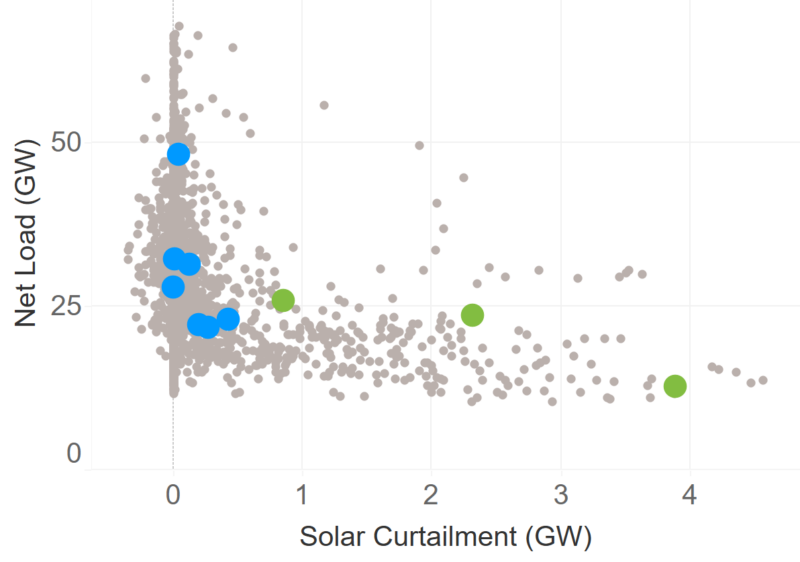

First, and perhaps most obviously, the weather impacts renewable generation and demand, and when there’s too much of the former and not enough of the latter, renewable projects are curtailed. Net load (total load minus renewable generation) is a useful metric to highlight this behavior. Figure 1 shows solar curtailment as a function of net load for Q1 2024. It’s clear that as net load drops below 20 GW, solar generation starts to be curtailed, increasing quickly as net load reduces further. These grid-wide supply and demand balancing issues that lead to renewable energy curtailment also play out on a local level, caused by transmission constraints. Even if there’s enough demand overall on the grid, if the renewable energy is located behind a transmission constraint, curtailment will still happen. Finally, there’s the tax incentives – wind projects tend to receive the Production Tax Credit (PTC) while solar projects tend to receive the Investment Tax Credit (ITC). Since the PTC is earned on a per megawatt-hour basis, many wind projects continue generating even when wholesale prices are negative. On the other hand, ITC-qualified solar projects will curtail as soon as wholesale prices become negative.

Figure 1: Net Load and Solar Curtailment, January – March 2024. Record-breaking periods shown in blue, missed records shown in green.

So, in terms of setting solar generation records, there needs to be an alignment of these variables – high solar generation potential, relatively low wind generation, relatively high load, and no meaningful transmission constraints. Figure 2 shows two days in February with different conditions and different outcomes. The first is February 19th, when there were favorable conditions and a new record was set – the skies were clear, wind output was low during the day, and net load stayed above 20 GW. A few days later on February 24th, conditions were not as favorable – skies were clear in the morning, but wind output was increasing and net load dropped below 20 GW. This meant solar projects were curtailed and while a new solar generation record 300 MW above the February 19th level could have been set, it was not.

Figure 2: Actual and Uncurtailed Solar and Wind on February 19th, 2024 (left) and February 24th, 2024 (right) Compared to Net Load (load minus actual wind and solar generation).

It’s also important to note the seasonality in these trends. The time of year makes these solar output records more unlikely – the first quarter of the year tends to be windy and load levels are on the low side too. As the summer approaches, wind generation will be lower on average and load will be higher. More solar projects will also likely be commissioned by then, so expect more records to be broken (and perhaps more frequently). Looking further forward, it will be interesting to see if some of the new solar projects elect for Production Tax Credits and therefore start to operate during periods of negative prices. If so, expect even more records to be set.

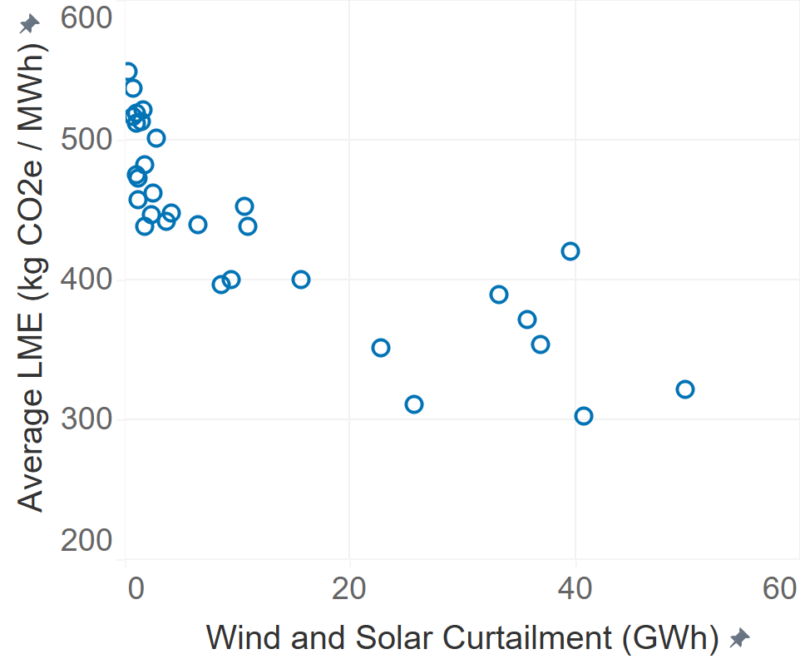

However, lost generation due to curtailment isn’t all doom and gloom. By definition, renewables make up a large proportion of the grid’s generation during periods of low net load and curtailment. For corporate buyers measuring their impact in emissionality terms, this means the ‘lost’ emissions impact due to curtailment is relatively small – most of that curtailed energy would have displaced other clean fuels (rather than fossil generators). This is especially true during periods of low net load, where high wind generation will keep marginal emissions rates low regardless of the level of solar curtailment. Figure 3 shows the average ERCOT Locational Marginal Emissions rate declining as renewable energy curtailments increase.

Figure 3: Daily Average ERCOT LME (kgCO2e / MWh) and Renewable Energy Curtailment in January, 2024.

As always with power markets, there’s a lot more going on behind the headlines of record breaking solar output.

In addition to downloading the report, you may want to watch a recording of a webinar on the Q1 report that we hosted in May, with the editor, Carl Ostridge, and lead analyst, Devon Lukas. They shared findings, insights, and hosted a live Q&A.

A view of Q4 2023 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. Please fill out the form to access the full report, the Editor’s Note is below.

Devon Lukas Lead Analyst Senior Analyst, Analytics Services

Carl Ostridge Editor SVP, Analytics Services

Emissions (Rates) Ignore (ISO) Borders

As of the end of 2023, Locational Marginal Emissions data is available for all seven deregulated ISOs in the U.S. That additional data coverage is reflected in the later parts of this report. Here, we’re going to dig into what the data can tell us about the current state of the different ISOs and how it can shine a light on the current hydrogen-hourly matching debate.

All the data included in this analysis is for the period November 2022 – October 2023.

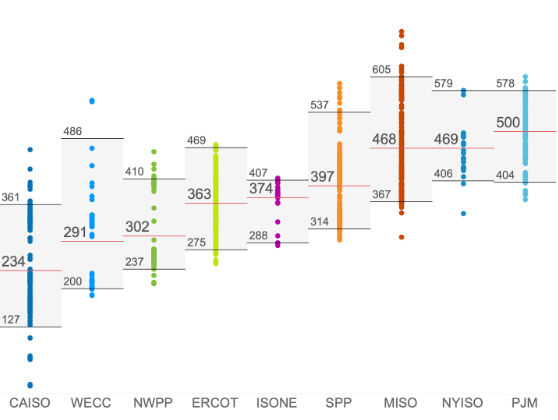

1. Renewables projects in CAISO, and particularly solar, had the lowest environmental impact.

There’s already a lot of solar power installed in California, and that means during the day when the sun is shining, solar power is often the marginal generator. That means incremental solar generation is displacing clean megawatt-hours from other solar projects, not fossil-based generators. The average renewable energy project in CAISO during this 12-month period displaced only 234 kgCO2e/MWh. That’s less than half the emissions impact of the average renewable energy project in PJM.

Figure 1: Locational Marginal Emissions Rates for wind and solar projects (kgCO2e/MWh), November 2022 – October 2023. Average, P5 and P95 values are shown.

2. PJM is where renewable energy has the biggest environmental impact.

A combination of relatively low penetration rates for renewables and fewer transmission constraints means there’s an outsized impact for any new wind or solar project in the PJM footprint because it is often displacing fossil-based generators and rarely displacing other renewables. On average, a renewable energy project in PJM displaced 25% more CO2 than an equivalent project in SPP and almost 40% more than projects in ERCOT.

3. There is a huge range of emissions rates within most ISOs.

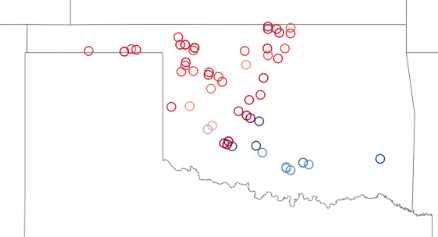

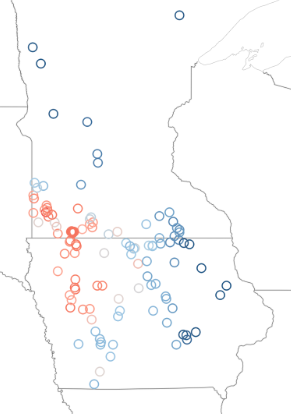

It’s perhaps more intuitive to make sense of the differences in average emissions impacts between ISOs – each has its own unique generation stack, load profile, and set of connections with neighboring regions, resulting in different emissions rates for renewables. However, there’s an even bigger range of emissions rates within these regions. This is primarily driven by the unique local transmission constraints within each region and how each of these constraints affects the ability of renewable generation to meet load. Two examples of localized variability in emissions impact are shown in figures 2 and 3. In both southern Oklahoma and western Minnesota, the emissions impact of wind projects is reduced due to local transmission constraints and congestion.

Figure 2: Locational Marginal Emissions, Oklahoma Wind Generators, November 2022 – October 2023.

Figure 3: Locational Marginal Emissions, Iowa and Minnesota Wind Generators, November 2022 – October 2023.

This last point about intra-regional variability is interesting for a number of reasons, but one to specifically call out here is the current debate around the IRS guidance for hourly matching of renewables for hydrogen electrolyzers under Section 45V of the Internal Revenue Code. The latest IRS proposal requires hourly matching of electrolyzer consumption with renewable energy procured within the same ‘region’. While the hourly matching regions don’t precisely match ISO boundaries, they’re pretty close. Therefore, the intra-regional variation in emissions impact for renewable energy projects would likely translate directly to the real-world emissions associated with ‘green’ hydrogen. An electrolyzer could procure renewable energy from a high-performing project in the region and avoid a lot more carbon than the electrolyzer consumes. The more worrying possibility is the opposite scenario – buying power from an underperforming project could mean that the hydrogen produced is actually far from ‘green’.

In addition to downloading the report, you may want to register to attend a webinar on the topic on Wednesday, February 7 at 1pm ET with the editor, Carl Ostridge. He’ll share findings, insights, and host a live Q&A.

A view of Q3 2023 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. Please fill out the form to access the full report, the Editor’s Note is below.

Devon Lukas Lead Analyst Senior Analyst, Analytics Services

Carl Ostridge Editor SVP, Analytics Services

A Tale of Two Technologies

When I think of Southwest Power Pool (SPP) I think of wind. Wind met almost 40% of SPP demand in 2022 and new output records have been consistently set over the past couple of years. When I think of SPP I don’t think of solar, though. Solar met less than 0.5% of SPP demand in 2022. And I’ve always found that a little surprising considering the southern SPP footprint has some of the best solar resource in the country (ref: NREL). Maximum solar output this summer in SPP was only 30 MW higher than 2022 while the equivalent metric in ERCOT increased by more than 3,500 MW.

The abundance of wind generators and the lack of solar also means the two technologies look very different when considering two important metrics – the monetary value and the decarbonization impact of each MWh.

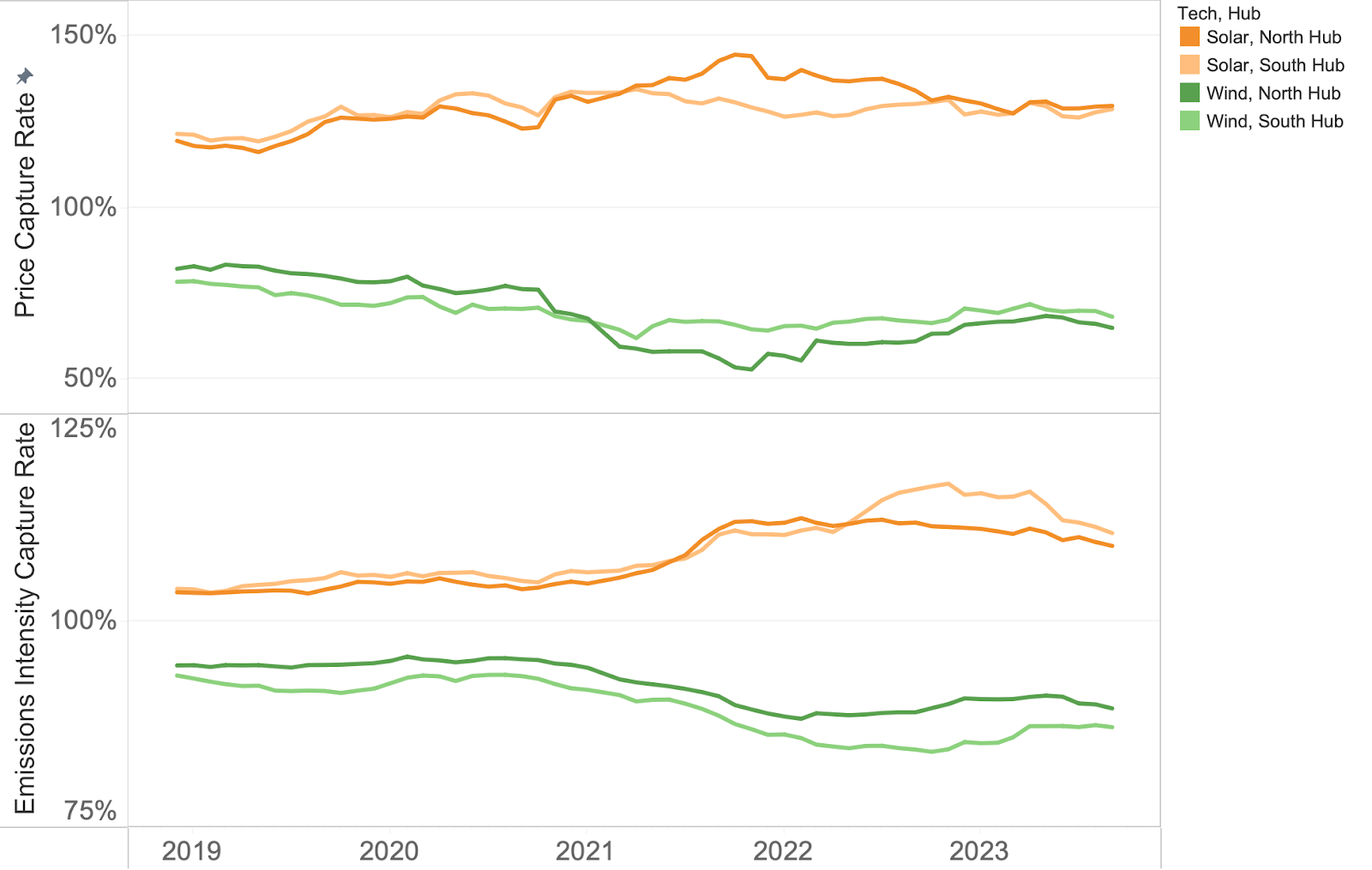

Figure 1 shows the capture rates (the value of the wind or solar-weighted MWh compared to around-the-clock MWh) for both price and emissions intensity. We see similar trends in both – wind is capturing less and less of the available monetary value and avoiding less and less CO2 while the opposite is true for solar.

Figure 1: Price and Emissions Intensity Capture Rate, 12-month rolling average. Uses representative modeled wind and solar generation data. February 2021 excluded.

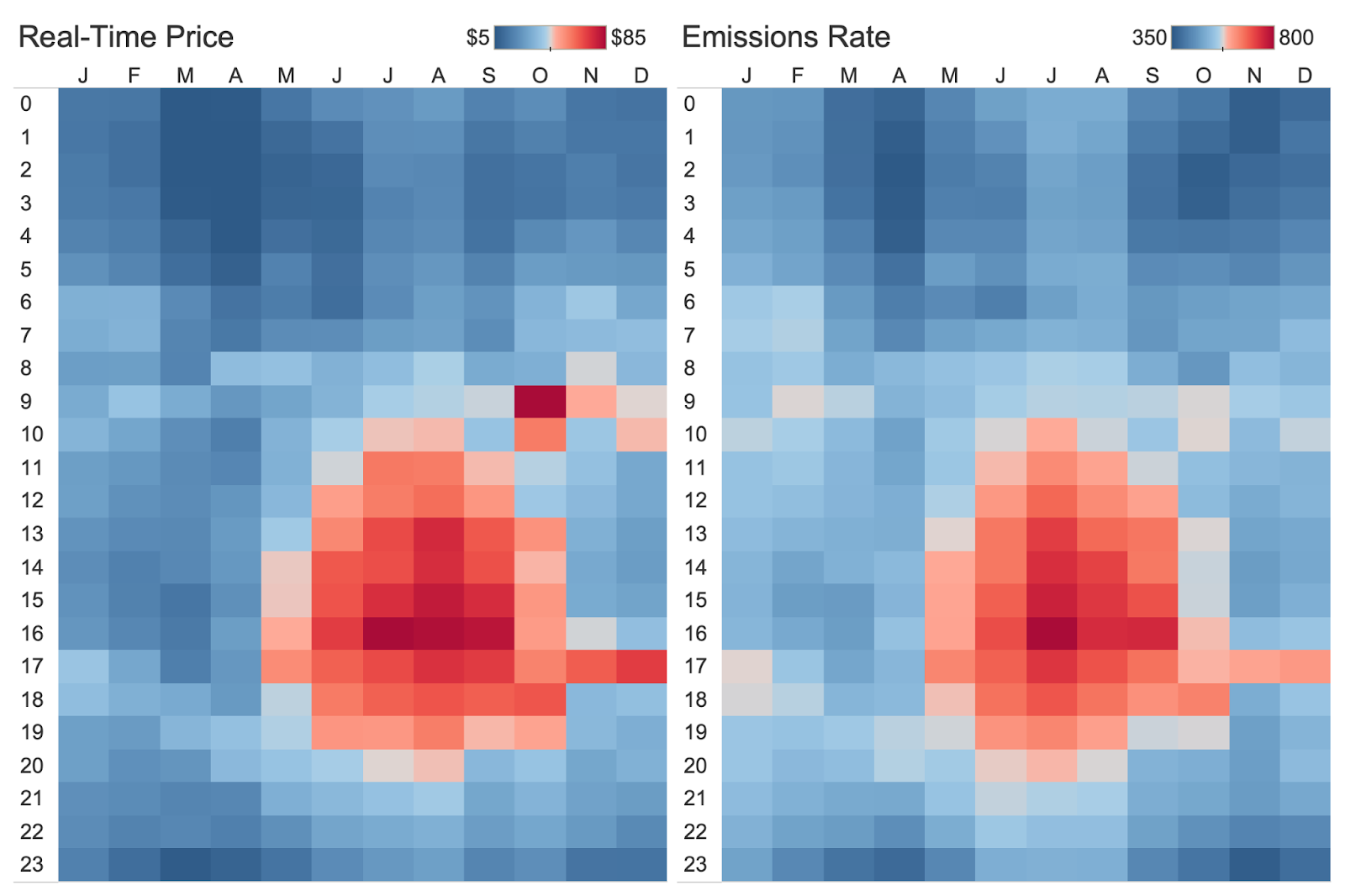

To understand what’s causing this we can look at the month-hour average prices and emissions rates over the past four years. We see that both prices and emissions rates are highest during the summer afternoons. During these times load is high and often wind output is low, meaning the marginal unit is a thermal generator with higher emissions rates. Of course, these are the same hours when solar output is peaking and that correlation leads to high solar value (in $ and CO2 avoidance terms) compared to an around-the-clock generation profile. Conversely, the low prices and low emissions rates are occurring (not coincidentally) in hours of high wind output and this drives the prices and emissions rates lower.

Figure 2: Average Real-Time Price and Emissions Rate 12×24, SPP South.

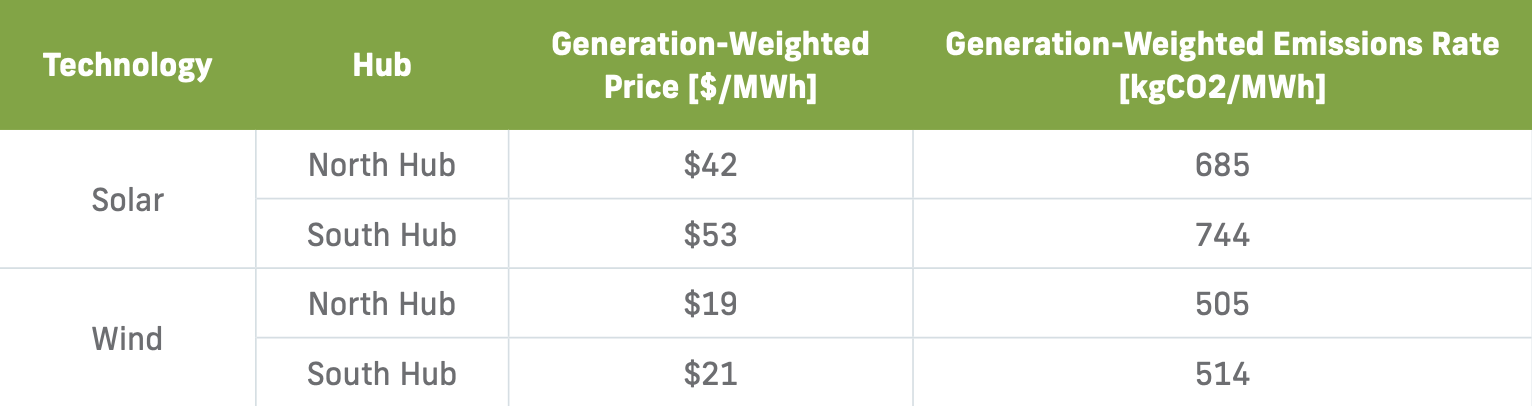

On the face of it, this means adding solar to SPP would be a win-win, it would capture relatively high value power prices and would displace thermal generators more often, avoiding more carbon emissions. In Q3 of this year, solar was worth more than $50/MWh at South Hub while wind was worth closer to $20/MWh. During the same period, solar generation also had a 40% larger emissions reduction impact compared to wind.

Table 1: Price and Emissions Values for Wind and Solar in Q3 2023.

So why aren’t more solar projects being built? There are a number of challenges, but transmission is a considerable one. The interconnection queue is long and growing thanks to the IRA, and getting an interconnection agreement often requires developers to share large upgrade costs. Further, this analysis reflects the hub values for prices and emissions. Wind projects in SPP suffer some of the worst price basis in the country with some projects seeing $10-20/MWh annual nodal discounts vs. the hub. Investment tax credit (ITC)-qualified solar projects would likely need to curtail output as soon as prices reach negative territory while production tax credit (PTC)-qualified wind projects tend to continue operating far beyond that point.

There’s currently value available for solar in SPP but only if project developers can navigate the complex issues related to transmission, interconnection, and congestion.

A view of Q2 2023 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. We use our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of locations and summarize key findings here. All of the data behind this analysis is curated by REsurety’s team of experts and available via our software products. It includes aggregated metrics for wind and solar projects operating in the U.S. All summaries are calculated using hourly-level data, and all energy-weighted price metrics are calculated using concurrent weather-driven generation and energy price time series. Please fill out the form at the bottom of the page to access the full report, the Editor’s Note is below.

June in Texas: High Heat, Not So High Power Prices

I recall the buzz during the summer of 2019 when power prices in ERCOT reached $9,000/MWh for a few hours and the speculation about how prices may have been lower with more solar on the grid. Fast forward to 2023. The hot topic to start the hot summer is instead how power prices may have been even higher without the observed solar generation. Solar energy’s contribution to grid resilience during this summer’s heat waves has even become mainstream news, with headlines about the absence of the power supply scares of previous summers.1

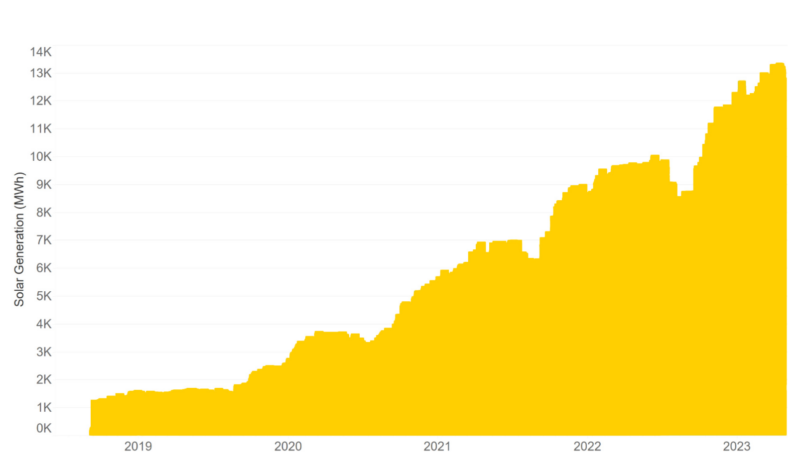

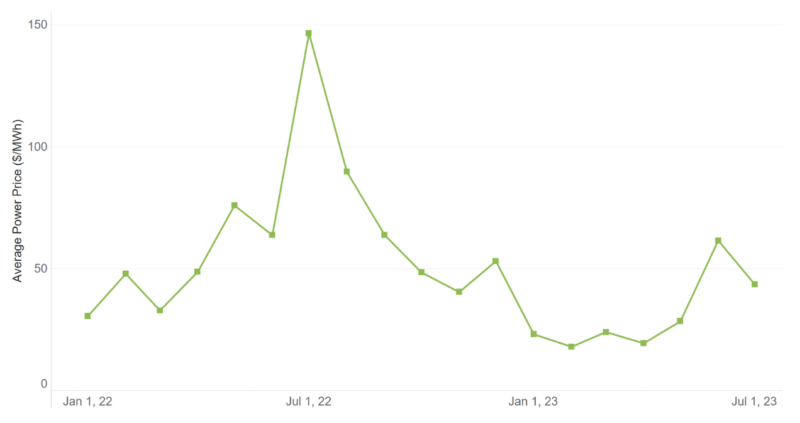

Indeed, solar capacity in ERCOT has grown over the last few years. Observed hourly solar generation regularly approached 13,000 MWh heading into this summer, compared to a maximum of approximately 10,000 MWh the same time last year (Figure 1). However, despite record breaking demand and a few hours of scarcity prices in June, the average monthly prices remained below the values from last summer (Figure 2). The average power price in June 2023 at ERCOT North Hub was $2 less than in June 2022 despite exceeding the monthly peak demand record by over 4,000 MW.2

Figure 1: Observed Hourly Solar Generation in ERCOT

Figure 2: Average Monthly Power Prices at ERCOT North Hub.

REsurety estimates that the average power price in ERCOT this June would have been nearly double the observed value without the additional solar generation. We also estimate that solar resources would have captured 27 percent more of this higher average monthly price, while wind resources would have captured 14 percent less.

Continued growth in solar capacity is expected to further degrade the capture rates for solar in ERCOT, while supporting capture rates for wind and keeping average prices lower for consumers. REsurety’s Weather-Smart fundamentals power price model shows reductions in solar value as solar buildout ramps up and the highest price hours are pushed out to the early mornings and evenings. At the same time, the reduction in power prices during afternoon hours also helps to limit downside risk to wind generation value. The lowest wind capture rates tend to occur in months that experience periods of low wind resource coinciding with periods of high demand from high temperatures.

We continue to watch how solar energy resources will perform with more hot weather still to come. Regardless of how the rest of this summer turns out, the impact that increasing solar penetration is having on markets like ERCOT is already apparent, and increasingly suggests that the near future is fundamentally different from the recent past. We will keep sharing our data findings in these quarterly reports as well as trends and thought leadership on our corporate blog.

Harnessing Batteries and Carbon Contracts to Accelerate Grid Decarbonization, authored by Tierra Climate in partnership with REsurety

This paper examines the economic carbon impact of compensating batteries for carbon reduction using detailed electricity emissions data and a carbon contract. Carbon contracts with grid-scale batteries might provide corporations with an elegant solution to meet sustainability targets and decarbonize the electricity grid, which cannot be accomplished through renewable energy purchases alone.

In partnership with REsurety, the paper leverages REsurety’s Locational Marginal Emissions dataset as part of the calculating mechanism.

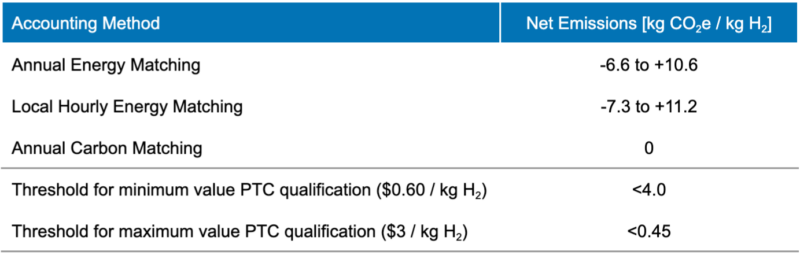

REsurety uses Locational Marginal Emissions (LMEs) data to analyze the effectiveness of the three carbon accounting methods proposed for compliance with new production tax credits available for clean hydrogen under the Inflation Reduction Act (IRA). This analysis considers 32 electrolyzer-renewable project pairs across 3 different grid regions (ERCOT, PJM, and CAISO) using hourly emissions and generation data from 2022. Seen in Table 1 below, the results show that, due to the difference in carbon intensities on the grid based on location and timing, determining “clean” hydrogen using Annual Energy Matching often results in significant increases in emissions despite the procurement of an equivalent quantity of energy from offsite clean energy to match the electrolyzer’s consumption. Further, Table 1 shows that while Local Hourly Energy Matching can help reduce net emissions in some locations, the impact of local transmission constraints often results in significant increases in net emissions even after energy is “matched” by hour. Finally, the Annual Carbon Matching method, using LME data, can ensure low or zero net emissions and qualification for the clean hydrogen production tax credit. The Annual Carbon Matching method also helps to incentivize development of electrolyzers in locations with cleaner grids with lower existing marginal emissions and the procurement of renewable energy in locations with dirtier grids and higher existing marginal emissions, therefore maximizing the ‘greening of the grid’ impact of the IRA legislation.

Table 1: Net emissions ranges for the three proposed accounting methods.

Fill out the form to access the full paper and accompanying resource.

A view of Q1 2023 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. We use our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of locations and summarize key findings here. All of the data behind this analysis is curated by REsurety’s team of experts and available via our software products. It includes aggregated metrics for wind and solar projects operating in the U.S. All summaries are calculated using hourly-level data, and all energy-weighted price metrics are calculated using concurrent weather-driven generation and energy price time series. Please fill out the form at the bottom of the page to access the full report, the Editor’s Note is below.

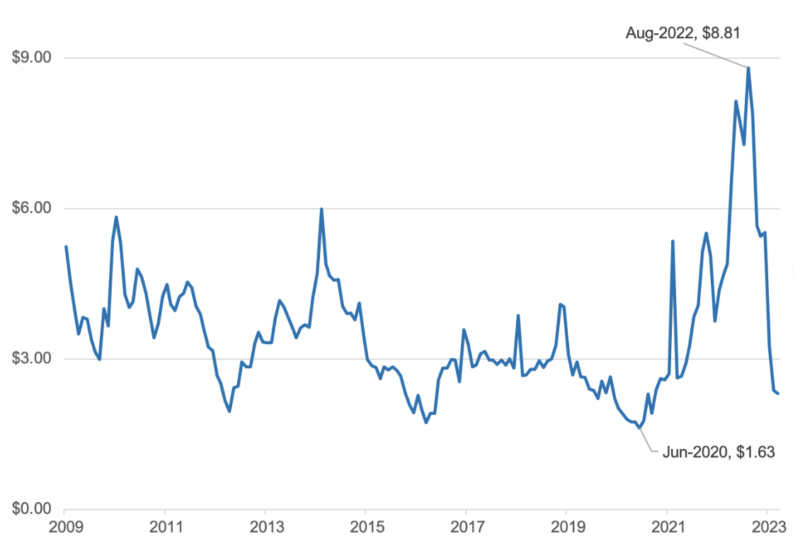

For me, the story of 2022 was the high average power prices across the U.S. Emphasis on average because the high prices were not driven by individual large weather or market events like Winter Storm Uri in 2021. Yes, there were some weather-linked events, but these really didn’t move the needle at the annual level. The real driver in 2022 was the underlying price of natural gas – Henry Hub prices started the year at ~$4/MMBtu (already high compared to the last few years) and peaked close to $9/MMBtu in the summer. That’s by far the highest natural gas price seen in the post-shale era of the last 14 or so years.

Figure 1: Historical Henry Hub Natural Gas Spot Prices ($/MMBtu).

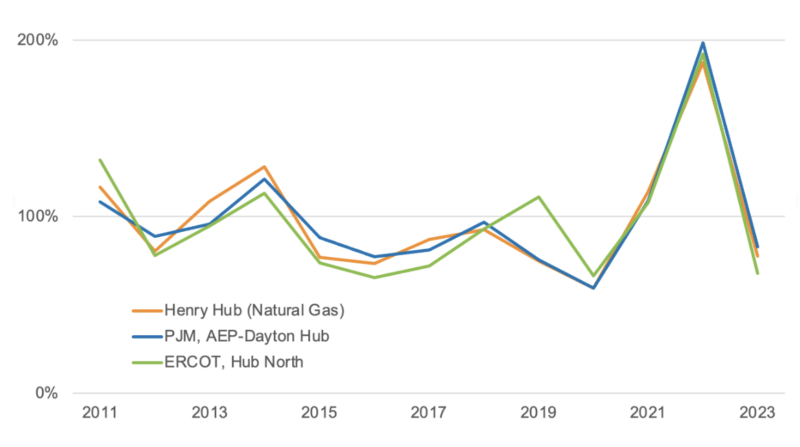

Natural gas is often the marginal fuel in many regions and there’s a strong correlation between natural gas prices and power prices as shown in Figure 2. The historic natural gas prices during 2022 also resulted in power prices reaching their highest annual average in at least the last decade (Winter Storm Uri’s influence in February 2021 excluded).

Figure 2: Natural Gas and Power Prices indexed to 2011-2022 averages (Feb 2021 excluded).

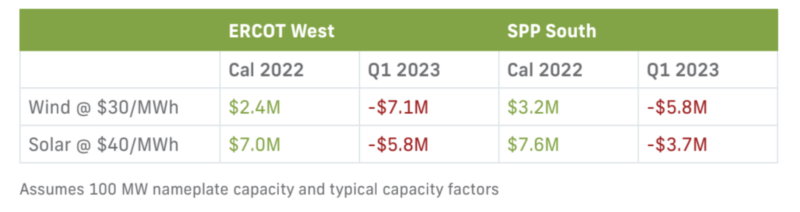

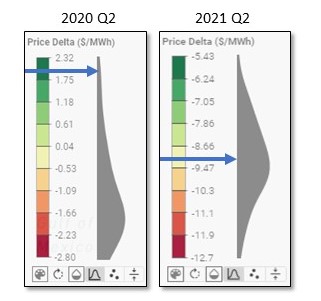

Those high prices led to large payouts to merchant projects and clean energy buyers. For example, a typical 100 MW wind project with a $30/MWh PPA settling at ERCOT West would’ve paid more than $2M to their buyer by the end of the year. An equivalent vPPA settling at SPP South would’ve paid out more than $3M.

Now, fast forward to Q1 2023 and the world looks very different. Gas prices have dropped more than 50% compared to Q4 2022 and 40% compared to Q1 2022. Power prices in most markets have seen similar decreases, down 20-50% compared to Q1 of last year. That means the same vPPAs that were paying large sums to buyers throughout 2022 are now back to paying the projects. In some cases, buyers cut checks to projects in Q1 that exceeded the checks that they received during the whole of 2022.

Table 1: Example Wind and Solar vPPA settlements for calendar year 2022 and Q1 2023

The volatility seen in commodity and power markets in the past 18 months is expected to continue. Natural gas fundamentals, new generation interconnection, supply chain challenges, geopolitical turmoil, and increasingly extreme weather are expected to continue causing large ups and downs in the markets and that, of course, means ups and downs for those buying and selling power.

To understand the contributions of the three primary drivers of changing prices and volatility – grid composition, commodity prices, and weather – REsurety publishes Weather-Smart fundamentals power price forecasts each quarter. For the next 20 years the forecasts account for multiple commodity scenarios and for each of those scenarios models how the grid and market will reach under weather conditions representing each of the past 40 years. For example, we forecast this summer’s prices under ‘mid’, ‘low’, and ‘high’ gas scenarios and if the heat of 2011 or the relatively mild weather of 2007 was repeated (and every set of summer conditions in between). This provides a unique view of how both the commodity prices and weather drive market outcomes.

The model predicts there’s approximately a 3x range between the highest and lowest prices averaged for the remainder of 2023. That’s the difference between having a vPPA pay out to the buyer at similar levels to 2022 or continue to pay out to the project in line with Q1 of this year. With this level of volatility, the clichéd investment disclaimers certainly ring true – “past performance is not a guarantee of future performance and prices may go up as well as down.”

At REsurety we’ll be keeping a close eye on how both the commodity markets and weather unfold over the coming months and keeping our Weather-Smart forecasts up to date with the latest data.

A Comparison of Strategies for Tackling Corporate Scope II Carbon Emissions, published by Tabors Caramanis Rudkevich

The purpose of this paper is to provide a comprehensive, comparative study covering a variety of factors impacting the cost and implementation of corporate clean energy procurement strategies.

Global climate change has pushed carbon emissions to the forefront of public scrutiny and scientific inquiry. Striving to reduce their net carbon footprint, large energy consumers have increasingly turned to renewable energy resources. These energy consumers have pioneered different approaches toward clean energy procurement, such as the RE100 initiative, Google’s 24/7 Carbon-Free Energy, Microsoft’s 100/100/0 vision, and the Emissions First partnership led by Meta and Amazon. This white paper examines different clean energy procurement strategies in terms of overall cost and effectiveness in carbon emissions reduction.

Using locational marginal emission rate (LMERs), we quantify the cost and carbon emissions impact of clean energy procurement strategies for corporate energy consumers with varying load shapes and within a variety of balancing authorities. We compare energy matching strategies against a strategy that directly accounts for carbon emissions, which we call carbon matching, for two different types of large electricity consumers in 5 different balancing authorities. Balancing authorities ranged from large ISO/RTOs (PJM and CAISO) to vertically integrated utility regions covering a regional (Duke Energy Carolinas) or municipal area (Los Angeles Department of Water and Power and Portland General Electric).

The results show the following:

Carbon matching, a strategy that directly accounts for carbon emissions using LMERs and ensures that avoided emissions are equal or greater than emissions attributable to load, is more cost-effective than any of energy matching strategies analyzed;

Energy matching does not guarantee reaching carbon neutrality;

Localized energy matching decreases carbon displacement efficiency;

Local energy matching may not be practical in certain regions, which could deter participation;

Hourly energy matching is the least efficient strategy at displacing carbon emissions, and its cost varies greatly depending on location

If you’d like to learn more about REsurety’s Location Marginal Emissions (LMEs) offerings, please contact us.

“LME is an important tool in assessing individual projects because seemingly identical renewable energy projects can have drastically different impacts on avoided carbon emissions.”

CarbonCount is a decision tool that evaluates investments in U.S.-based renewable energy, energy efficiency, and climate resilience projects to determine how efficiently they reduce CO2 equivalent (CO2e) emissions per $1,000 of investment. CarbonCount produces a quantitative impact assessment for investments’ carbon avoidance by integrating forward-looking project assumptions, emissions factors, and capital investment.

This white paper explains why CarbonCount matters, why it’s being updated, the methodology behind it, and use cases. REsurety’s Locational Marginal Emissions (LME) data is also featured in the paper.

Learn more here, or download the full white paper below.

A view of Q4 2022 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. We use our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of locations and summarize key findings here. All of the data behind this analysis is curated by REsurety’s team of experts and available via our software products. It includes aggregated metrics for wind and solar projects operating in the U.S. All summaries are calculated using hourly-level data, and all energy-weighted price metrics are calculated using concurrent weather-driven generation and energy price time series. Please fill out the form at the bottom of the page to access the full report, the Editor’s Note is below.

Carl Ostridge SVPof Analytics Services

Editor’s Note:

For Renewables, Timing is Everything

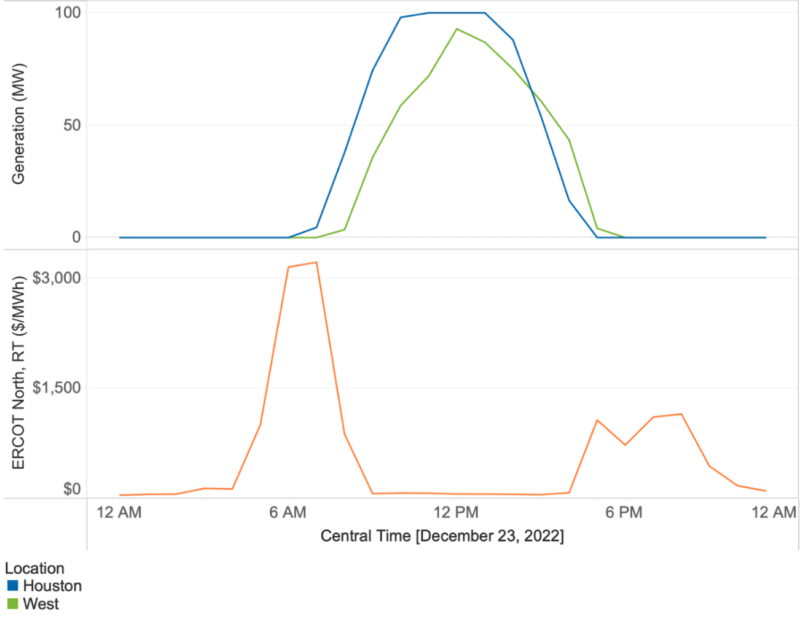

The final quarter of 2022 closed out with some extreme weather across most of the country and while lots of comparisons were quickly drawn against 2021’s Winter Storm Uri, December of 2022 also provided useful insights into the changing dynamics of power markets as renewable energy penetration rates increase. While the impact on market prices was smaller overall compared to Uri, one of the most interesting outcomes from the winter weather was present in ERCOT and highlighted the fact that timing is everything when it comes to capturing value from renewable energy assets.

The map in Figure 1 shows the “capture rate” potential of solar assets across the ERCOT footprint in December, 2022. Capture rate is the ratio of generation-weighted price and simple average price during the period in question and shows how much of the average price is ‘captured’ by, in this case, solar assets. Immediately visible is the interesting geographic trend across the ERCOT footprint, with the highest solar capture rates occurring in the east and west extremities while the lowest capture rates occur in the center. To understand what’s driving this, we need to look at the underlying data for one specific day.

Figure 1: Solar Capture Rate at ERCOT North Hub RT, December 2022

Figure 2: Modeled Generation for 100MW Solar Assets Located in the Houston and Midland Regions & Market Prices, December 23rd, 2022

Figure 2 shows the hourly average real-time market prices on December 23rd, 2022 as well as the generation of two hypothetical solar assets; one in west Texas and another close to the Houston area. The highest prices during this day occurred early in the morning and in the evening, meaning that most of the solar output during December 23rd did not coincide with the high prices. This leads to the very low overall capture rates in December, ranging from ~45-60% across ERCOT. But importantly, the lower prices during the day are not actually a coincidence – peak solar output has more than doubled since 2020 and there was approximately 8 GW of solar generation during the middle of the day on December 23rd, 2022, enough to move the grid out of scarcity pricing mode and back to more “normal” prices. This dynamic also creates values for locations with early sunrises (in the east) and late sunsets (in the west). The difference in sunrise and sunset times in Midland and Houston on December 23rd was approximately 30 minutes, but that was enough to secure an additional $50/MWh of value. Solar assets located close to Houston would have been able to capture the value of the high market prices before the sun came up on most of the existing solar assets further west and prices fell. That $50/MWh difference might not sound like a lot, but considering that solar capacity in ERCOT is predicted to exceed 20 GW by 2025, this type of ‘duck curve’ where solar generation serves to systematically reduce prices during the day is likely to happen with increasing frequency. Therefore, siting solar assets in locations able to naturally take advantage of the ramp hours may become increasingly valuable.

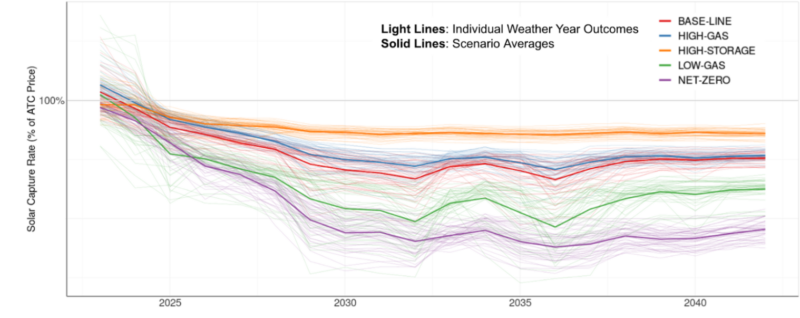

Finally, this shift in ERCOT’s grid mix, price dynamics, and subsequent drop in solar capture rates is predicted by REsurety’s Weather-Smart Fundamentals modeling. REsurety models ERCOT’s grid in 5 different future states, including high storage and net zero, and computes outcomes based on weather data representing the past 40+ years to derive the data in Figure 3 below.

Figure 3: ERCOT Solar Capture Rates Predicted by REsurety’s Weather-Smart Modeling

The average solar capture rate in ERCOT is forecast to drop below 100% by 2024, driven by the type of event we’re highlighting here – solar generation is high enough to reduce prices during the day and scarcity pricing is moved to the early morning and evening hours. As ever, timing will be the key to renewable energy value.

A view of Q3 2022 U.S. renewable energy performance

REsurety creates the State of the Renewables Market report every quarter to provide readers with data-driven insight into the value and emerging trends of renewable generation in U.S. power markets. We use our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of locations and summarize key findings here. All of the data behind this analysis is curated by REsurety’s team of experts and available via our software products. It includes aggregated metrics for wind and solar projects operating in the U.S. All summaries are calculated using hourly-level data, and all energy-weighted price metrics are calculated using concurrent weather-driven generation and energy price time series. Please fill out the form at the bottom of the page to access the full report, the Editor’s Note is below.

Carl Ostridge SVPof Analytics Services

Editor’s Note:

Grid Congestion Hurts Project Economics & The Environment

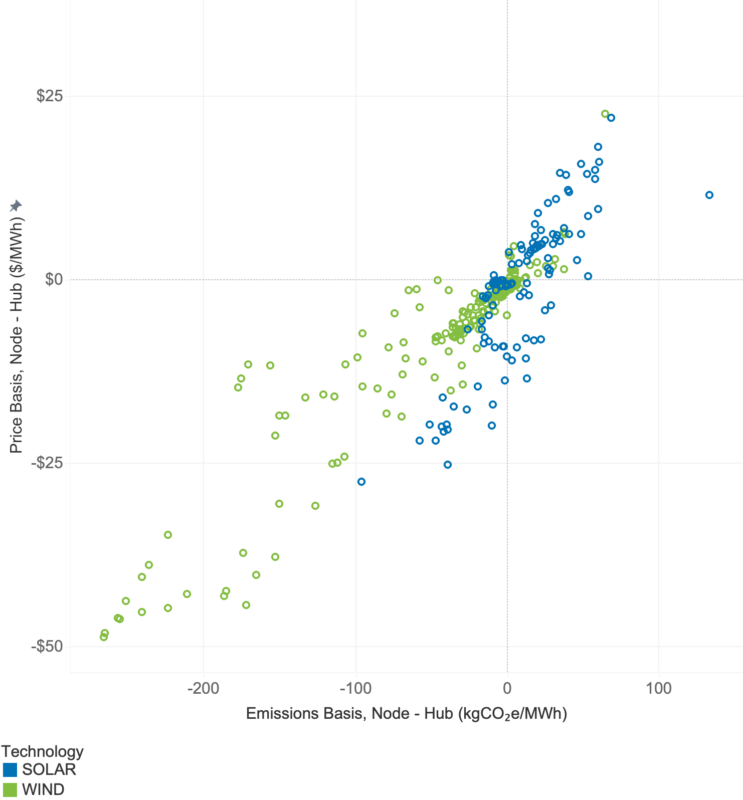

Project developers know well the perils of transmission constraints and grid congestion when it comes to their project’s economics. If you locate your project at a point on the grid with limited availability to move clean electricity to where it will be consumed, local power prices will be much lower than average prices across the wider grid. This phenomenon is often referred to simply as “basis” but we’ll be more specific here and call it “price basis”. Price basis is bad for project economics for two reasons – first, the project’s merchant revenue (the value of electricity sold to the system operator at the point of interconnection) can be vastly reduced and second, if the project enters into a financial agreement to sell their electricity at a hub price (an aggregate across a large grid area) they may end up owing large sums of money that their merchant revenue cannot support.

The magnitude of price basis is hard to predict and, without investment in transmission or energy storage, tends to get worse over time as more wind and solar projects are added to the grid in locations with high resource availability. Developers and consultants spend lots of time, money and effort building models to analyze historical basis and forecast future scenarios to decide where to build projects and inform their economic outlook.

However, the transmission constraints and congestion that drive price basis also lead to what we’ll refer to as “emissions basis”. When a transmission constraint binds in a region with plentiful wind and solar generators, incremental clean energy (behind the constraint) often curtails other existing clean generators rather than carbon-emitting thermal generators elsewhere on the grid. This leads to emissions basis – wind and solar projects subject to transmission constraints avoid fewer tons of carbon emissions per MWh generated than the grid-wide average. In the absence of additional transmission or energy storage infrastructure, building additional wind and solar facilities in these regions has a diminishing environmental impact. Each new facility contributes less and less to the ultimate goal of decarbonization.

Figure 1: Price basis vs emissions basis for wind and solar projects in ERCOT and PJM (Jan-Jul 2022)

The strong correlation between price basis and emissions basis is highlighted in the plot below. Each point represents a wind or solar project in ERCOT or PJM and the values of price and emissions basis is calculated for the period January to July 2022. It’s clear from the plot that the projects with the highest levels of negative price basis have the lowest environmental impact while those with positive price basis tend to displace significantly more carbon emissions from the grid. Of course, there are many nuances to the data beyond this high-level correlation – trends based on location, technology, time of day and season – that REsurety’s Locational Marginal Emissions data can expose.

REsurety calculates Locational Marginal Emissions values at the nodal level with hourly resolution to provide the information necessary for project developers, investors, and offtakers to make informed decisions about where to build or invest in new projects to maximize their revenues and environmental impact.

We’ve expanded this report to provide information on both the financial and environmental value of wind and solar generation in the U.S. We hope you find this report informative.

Updating Scope 2 accounting to drive the next phase of decarbonization

EXCERPT: Corporations are increasingly focused on reducing their carbon footprints by decarbonizing the electric grid. While solar and wind energy development have rightly been a mainstay of these efforts, there is growing consensus that producing more clean energy alone isn’t enough. To maximize grid decarbonization, clean generation needs to occur at times and locations where its output displaces the highest-emitting resources. Consumption timing and location should be adjusted to minimize its carbon emissions via siting decisions, demand flexibility measures, and energy efficiency. And energy storage is needed to manage grid congestion and mismatches between clean supply and demand.

Effective carbon accounting frameworks can help coordinate these complex mitigation strategies by allocating emissions among the entities responsible for producing them. These accounting frameworks attempt to ensure that activities with more impact on actual emissions have more impact on carbon accounts. Given the large and increasing interest of investors, customers, regulators, and governments in corporate decarbonization initiatives, effective carbon accounting frameworks can encourage corporations to maximize their actual carbon reductions.

REsurety creates the REmap-powered State of the Renewables Market report every quarter to provide readers with data-driven insight into the emerging trends and value of renewables in U.S. power markets. We combine our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of projects and locations and summarize key findings here. All of the data behind this analysis is available via our interactive software tool, REmap. Please fill out the form at the bottom of the page to access the full report, the Editor’s Note is below.

Blair Allen Director, Software Customer Success, REsurety

Editor’s Note:

Node to hub basis* is rapidly becoming one of the most prominent financial risks for renewable developers and clean energy buyers alike. Although not a new issue, it has recently become more visible for two reasons: first, it is getting much worse in many areas with a lot of renewables, and second, clean energy buyers are increasingly taking on basis-risk exposure through contractual terms in PPA agreements. While basis used to be a risk only borne by project developers and investors, now corporates are sensitive to it as well.

In Q2, a handful of renewable-rich regions saw generation-weighted (AsGen) basis worsen by double digit values relative to the 4 year Q2 average. In many cases this was most prominent in areas that were already no stranger to negative basis. In ERCOT South Hub, for example, the average AsGen basis for operating wind projects in Q2 over the last 4 years was -$11 – in 2022 it declined to -$34. In the NP15 region of CAISO, the average AsGen basis for operating solar projects dropped from -$9 over the last 4 years to -$27 in 2022. And in SPP South Hub, operating wind projects saw their 4 year average decline from -$9 to -$31 in 2022.

But hub-level average values only tell part of the story, since basis is inherently a project-specific concern and can vary considerably not only within hub boundaries but across projects only miles apart from each other. For instance, when considering the projects within SPP South Hub last quarter, REmap shows project-by-project AsGen basis values that varied from as low as -$48 to as high as $26. The same extreme divergence played out across different ISOs and hubs, driven by subregional constraints driving a wedge in value between locations on either side of congested areas.

Basis warrants so much attention because it is extremely volatile and has a large impact on investment returns. In addition, it is hard to solve: investment into transmission infrastructure takes years and is extremely expensive. Developers screen for viable greenfield locations to avoid it, investors pore over model results to price it, and now energy buyers are turning to their advisors or tools to understand it better as well. The basis risk sharing clauses increasingly present in PPAs link the developer and clean energy buyer to the project’s basis performance in ways the two groups weren’t before, and the mechanics of that linkage aren’t always well understood. Although its impact ultimately depends on the counterparty and the project-specific contract details that can either worsen or improve exposure, one thing is clear: basis should be on everyone’s radar.

In this Q2 REmap report, we analyze a number of metrics including: shape, capacity factor, and AsGen value of power for renewables domestically. REmap users have real-time access to these metrics and more, including basis analysis, through the map-based SaaS offering.

*AsGen basis is defined in this report as the difference between a project’s AsGen nodal price ($/MWh) and its hub price ($/MWh), where the hub is assumed to encompass the area where the node is located.

The hedge market is offering the same menu of options a year and a half after a sudden cold snap in Texas left some power projects facing huge losses.

However, more attention is being paid to how to cap exposure in extreme scenarios.

Winter Storm Uri was an extreme cold event in late February 2021, centered in Texas but also affecting neighboring states, that was a one-in-10-year or one-in-50-year event, depending on which meteorologist you ask. It was not off the charts, but it involved an extreme level of sustained cold. There were deaths and significant property damage in Texas.

The storm led to a spike in electricity demand, especially for heating, and a shortfall in supply.

The shortfall in supply was driven by a number of factors, but the main driver was power plants froze physically and transmission infrastructure was shut down. These factors affected all types of power plants. The most pronounced effect was on gas-fired generation, but renewables, and wind in particular, were affected as well.

There was a pronounced financial impact in ERCOT because of the mechanism within ERCOT to reward generation during spikes in demand. There are administrative adders to the spot electricity price that force the price of power to go to a cap, incentivizing supply when demand spikes. At the time, the cap was $9,000 a megawatt hour. The result was that a spot market in which the price for electricity is often in the $20 to $40 range per MWh, was suddenly pricing power at $9,000 a MWh for three days.

REsurety creates the REmap-powered State of the Renewables Market report every quarter to provide readers with data-driven insight into the emerging trends and value of renewables in U.S. power markets. We combine our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of projects and locations and summarize key findings here. All of the data behind this analysis is available via our interactive software tool, REmap. Please fill out the form to access the full report, the Editor’s Note is below.

"*" indicates required fields

Blair Allen Director, Software Customer Success, REsurety

Editor’s Note: As the first quarter of 2022 concludes, we reflect on historic highs and historic lows. Another record in ERCOT marks the quarter’s passing, just as one did a year ago following the market events of February 2021. However, unlike the soaring prices of last year, this record involves a prolonged period of negative pricing, and another turn in a developing plotline we commented on last quarter. Please fill out the form below to access the report.

Consider this comparison: in February 2021 ERCOT West Hub (along with others) settled at the market price cap of $9,000/MWh for three days; in February 2022 ERCOT West Hub saw a two day period where prices never rose above $0/MWh. Mild demand coupled with sustained periods of high wind and solar generation created the conditions for this negative pricing event, though these conditions weren’t isolated to only those few days. In fact, by the end of the quarter, West Hub would more than double the number of negative-priced hours than were seen in Q1 the year prior.

One impact of this increasing frequency in negative pricing is rising levels of curtailment, particularly among solar projects which, unlike wind, don’t benefit from the production tax credit and are less likely to operate below $0/MWh. For example, using the modeled energy in REmap, which tells us how projects could have performed based on underlying wind/solar resource availability, last quarter West Texas solar projects saw anywhere from 20 to 30% of their potential hourly production for a given month fall in negatively priced hours. However, in reality these projects weren’t operating at their potential capacity in these intervals, and either shut down or significantly ramped down production.

Another important angle to consider: whereas for the last few years hourly negative prices at West Hub were evenly split between on-peak and off-peak hours during this time of year, this year saw that balance shift to 60/40 in favor of on-peak hours. The cause for this shift is clear: increasing amounts of solar capacity means that low pricing is no longer just following the production profiles for wind, and is coinciding more regularly with the rise and fall of solar energy.

Looking ahead, as seasons change into summer conditions so too do we expect a change in the volume of negative pricing. An increase and shift in demand– which will steadily move more towards the mid afternoon as air conditioning ramps–and a decline in wind production at the same time should converge to steadily mitigate on-peak negative price frequency. Q2 will likely be a transitional period, with frequency of negative pricing hours remaining high to start before subsiding more materially by the end of the quarter.

The most innovative companies worldwide choose Akamai to secure and deliver its digital experiences – helping billions of people live, work, and play every day. With the world’s largest and most trusted edge platform, Akamai keeps apps, code, and experiences closer to users – and threats farther away.

With REsurety’s locational marginal emissions (LME) data, Akamai is able to be far more accurate in its avoided emissions calculations. Instead of trying to make sense of inconsistent regional datasets, Akamai is able to calculate the precise impact of its activities at each location on the grid. In addition, REsurety’s project LME reports provide visibility into why emissions are what they are – for example, showing how much gas or coal is being displaced, or how much wind is being curtailed due to Akamai’s activities. Lastly, Akamai is now able to use the LME data to evaluate new PPA opportunities to ensure that it is focusing its efforts on the locations and technologies that can have the biggest impact on carbon emissions. Learn more by downloading the case study.

“…LMEs bring the environmental community five steps closer to the measurement accuracy needed to solve the global emissions crisis.”

– Mike Mattera, Director of of Corporate Sustainability and ESG Officer, Akamai Technologies

Authored by Jennifer Newman, Vice President of Atmospheric Science Research, REsurety

White Paper Executive Summary

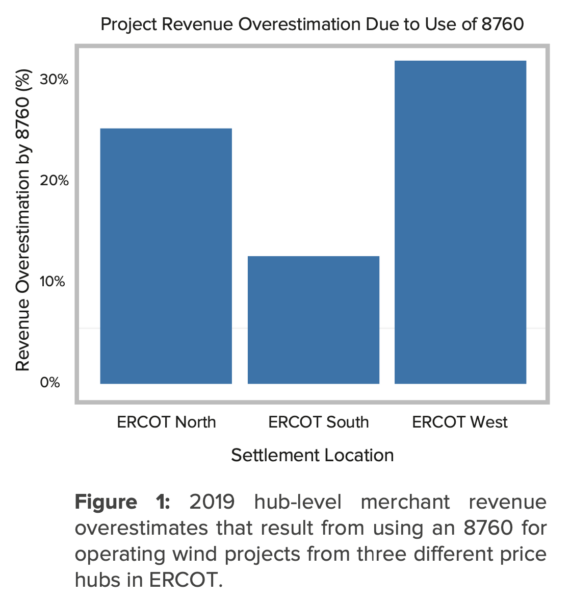

An “8760” (sometimes known as a “typical meteorological year,” or “TMY”) is a year-long hourly time series of expected generation for a wind or solar project. As the name implies, an 8760 contains generation values for all 8,760 hours of a year (non-leap year) and captures the typical seasonal and diurnal generation patterns at the site. Despite their widespread use in the renewable energy industry, there are two particular use cases of 8760s that can lead to significant errors in revenue estimation: 1) the pairing of an 8760 with a non-concurrent price time series and 2) the use of an 8760 as an input to a forward-looking price model.

The first, pairing an 8760 with non-concurrent prices, misses the impact of hourly wind and solar generation on market price, which can be particularly significant in markets with high renewable penetration. For example, Figure 1 demonstrates that pairing an 8760 with non-concurrent ERCOT power prices results in annual wind project revenue overestimates that can exceed 30%.

The second use case, using an 8760 generation profile as an input to a pricing model, does allow the user to capture the impact of hourly renewable generation on market price, if modeled correctly; however, the resulting distribution of forecasted prices will only represent the impact of a single, “normal” weather year. In reality, renewable energy projects will experience a variety of weather conditions, with non-typical weather years having an asymmetric and sometimes extreme impact on the price of power.

In this paper, we use observed and modeled data to quantify the impact of using an 8760 for renewable energy project value estimation, with a primary focus on wind generation. We demonstrate that pairing an 8760 with non-concurrent prices results in consistent wind project value overestimates in markets with significant wind penetration. We also show that using an 8760 to drive a forward-looking price model leads to a condensed price distribution that misses extremes and is not representative of historical price distributions.

Please fill out the form below to access the entire white paper.

Measure and Maximize the Carbon Impact of your Load and Clean Energy Purchases with Confidence

Download REsurety’s product brochure on Locational Marginal Emissions to learn more about the product offerings and uses of this innovative, carbon-tracking technology.

Download the Weather-Smart Fundamentals Modeling Product Brief to learn about REsurety’s fundamentals-based price model and the key benefits that it unlocks for users.

Risk Management Tools for Clean Energy Sellers and Clean Energy Buyers

This brochure outlines: REsurety’s Experience; Tools for Energy Buyers and Sellers such as power purchase agreements and settlement swap agreements. Fill out the form below to download.

Platts has extensive coverage of the US Renewable Energy Certificates (RECs) market with prices published across all compliance and voluntary state markets.

Not all RECs have the same emissions impact and crucially emissions impact is not currently reported for any REC. As a result, the carbon reduction potential of individual REC instruments is not captured in current pricing.

S&P Global Commodity Insights has partnered with REsurety to bring transparency to renewables based emissions impacts.

Broad Reach Power (BRP) is a leading U.S. utility-scale independent power producer (IPP) that understands the long-term value and rapid growth of energy storage as an infrastructure asset, particularly in those markets transitioning from traditional to renewable generation. BRP’s facilities provide flexibility, reliability, and environmental benefits while generating revenues from both risk-management contracts and spot-market opportunities.

“With a storage pipeline exceeding 20GW, granular carbon emissions data is mission critical in assisting Broad Reach Power more efficiently reduce carbon emissions while increasing grid reliability; REsurety provides that data.”

– Paul Choi, EVP of Origination, Broad Reach Power

Learn how Broad Reach Power uses REsurety’s Locational Marginal Emissions (LMEs) to measure impact, offer innovative solutions and identify project locations.

We sat down with Rich Santoroski, Strategic Advisor, and Raj Singamsetti, Market & Regulatory Lead of the climate investment firm HASI, to talk about how they use Discover to conduct investments in renewable projects.

With more than $8 billion in managed assets, HASI’s (NYSE: HASI) core purpose is to make climate positive investment with superior risk-adjusted returns. The company’s vision is that every investment should improve its climate future, which is why they require that all prospective investments are neutral to negative on incremental carbon emissions or have some other tangible environmental benefit, such as reducing water consumption.

“We use Discover in every deal because we trust it to help us to understand real world performance and to determine the appropriate value of an investment.”

REsurety creates the REmap-powered State of the Renewables Market report every quarter to provide readers with data-driven insight into the emerging trends and value of renewables in U.S. power markets. We combine our domain expertise in power markets, atmospheric science, and renewable offtake to analyze thousands of projects and locations and summarize key findings here. All of the data behind this analysis is available via our interactive software tool, REmap.

The REmap-Driven Q3 2021 State of Renewables Report was released today! This report reveals the captured value of operational wind and solar projects in major US markets in Q3 2021, and highlights how those values have changed in each market over time. Data is aggregated from millions of data points across public and private sources to shed light on the value of renewable generation.

REsurety sat down with Joan Hutchinson, Managing Director, Off-take Advisory, at Marathon Capital, to talk about how her team uses Discover to inform their corporate clients on renewable energy procurement.

ABOUT MARATHON CAPITAL: Marathon Capital is a world-class investment bank with a mission to achieve their clients’ strategic and financial objectives by delivering inspired, knowledge-based solutions to the clean power, sustainable technologies & infrastructure markets. Marathon Capital is a leader in transformational deals across the global clean energy landscape bringing over 20 years of renewable energy and clean technology experience.

Note: What was historically known as Project Explorer and Carbon Explorer is now referred to as Discover and Impact. What was historically known as the REsurety Platform is now referred to as CleanSight.

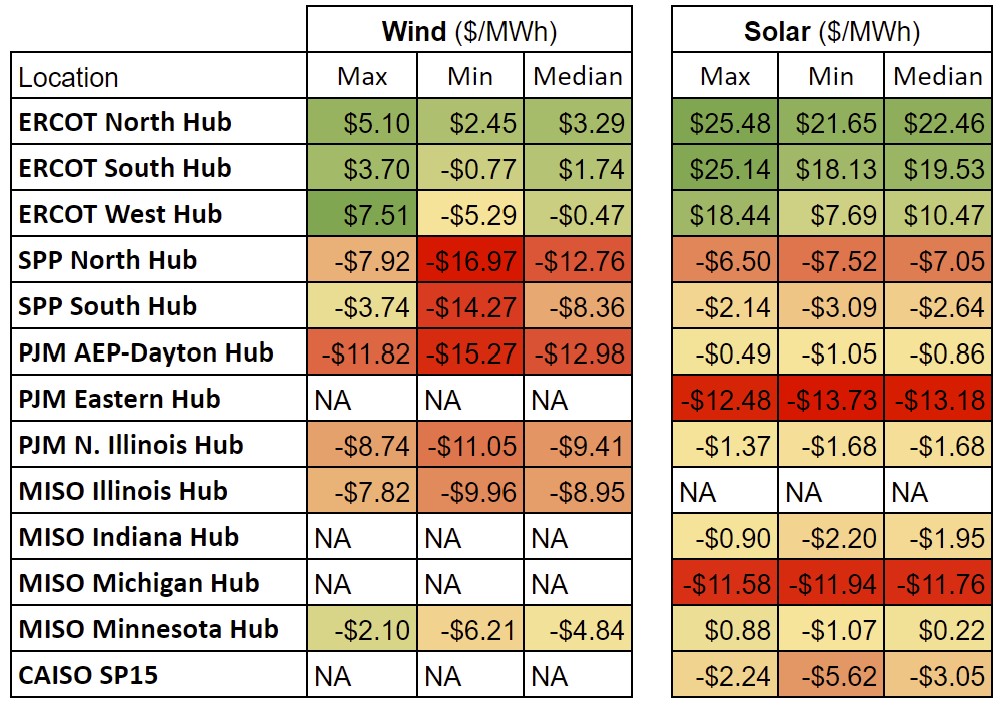

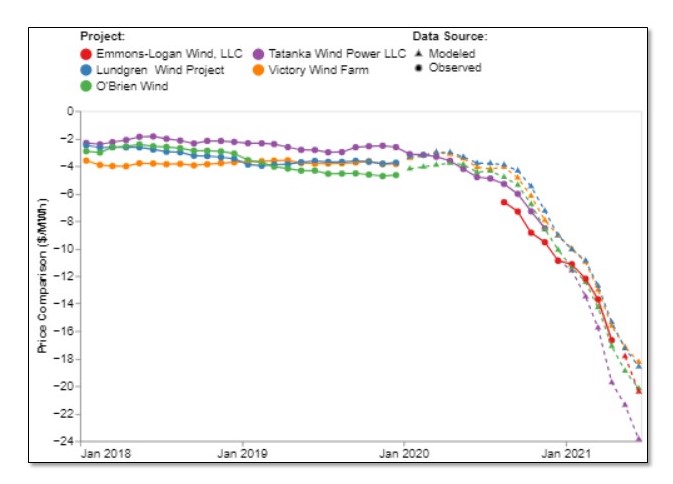

REmap’s new vPPA simulator feature allows users to backcast vPPA settlement at all project locations, enabling analysis of market performance through the lens of a generator or vPPA buyer.

vPPA settlements represent the value (or cost) of the unit-contingent contract-for-difference hedge settlements that result from a virtual Power Purchase Agreement (vPPA) with a project.

The results below show modeled¹ vPPA settlement values (in $/MWh) from the energy buyer’s perspective over the course of Q2. For potential vPPA buyers, this data answers the question: “If I signed a vPPA at prices available today, how would it have performed this past quarter?”

Modeled vPPA settlement outside of ERCOT generally resulted in a cost for the vPPA buyer, even assuming today’s competitive PPA prices². Within ERCOT, vPPA settlement favored the vPPA buyer, with settlement values surpassing $25/MWh at some Texas solar projects. The cost of purchasing renewable energy through a vPPA was greatest for energy buyers with a wind vPPA settling at SPP North Hub, SPP South Hub, or PJM AEP-Dayton Hub. Solar vPPAs were most costly for projects settling at PJM Eastern Hub or MISO Michigan Hub.

Q2 2021 Modeled vPPA Settlement for Energy Buyers

Figure 1: Q2 2021 Modeled vPPA Settlement for Energy Buyers. Values for locations/technologies with limited data are not shown or marked “NA”.

¹ Results use REmap data for operating projects, which includes modeled and observed hourly generation and observed market prices. Cell values represent the project with the maximum, minimum, or median project settlement value to an energy buyer for the quarter.

² vPPA prices used are from the LevelTen Q2 2021 PPA Price Index, which reports on PPA bids by hub and technology type.

2. Coastal Texas Wind Projects Join the Rest of the Pack

Coastal wind projects in Texas tend to experience higher wind speeds in the afternoon hours, which typically aligns well with afternoon periods of high demand and high power prices. The ability to generate during high priced afternoon hours means coastal projects typically benefit from a positive shape (also known as covariance), whereas wind projects in the rest of Texas tend to experience negative shape (i.e., hours of high generation are negatively correlated with hours of high power prices).